OASDI on Your Paycheck: What It Is & Why You Pay It (2025)

EmploymentBonica

December 26, 2025

This article is for you if you’ve ever opened your pay stub and wondered what that portion labeled OASDI is.

Everyone recognizes the usual deductions like Medicare or federal income tax, but that OASDI line just confuses people.

The acronym looks way too technical, the amount can seem kind of big, and most people have no clue where that money goes. That is exactly why you need a guide.

OASDI stands for Old-Age, Survivors, and Disability Insurance, and it’s what most people just call the Social Security tax.

Every time your manager gives you a paycheck, a small percentage is automatically held back to fund the Social Security program. This program is huge. It sends money to people who retire, people with disabilities, and the family members of workers who have passed away.

OASDI is a social safety net that you pay into throughout your career, and in return, it supports you and others when regular work income isn’t possible anymore.

OASDI is mandatory for almost everyone. Your pay stub might show one number, your employer pays a different amount, and if you’re self-employed, the rules change completely. Then you throw in things like annual wage caps and special exceptions.

A lot of employees just ignore the details, assuming it’s just one more deduction they can’t avoid. But knowing how OASDI works helps you make way smarter financial choices.

Table of Contents

What is the OASDI tax on a Paycheck?

Figuring out how OASDI is calculated is the key to understanding that number they take out of every paycheck. Although it may appear as just another line item on your pay stub, it follows a very specific formula.

The OASDI tax rate is 6.2%, and your manager kicks in an extra 6.2% on your behalf. When you put that together, it’s a total of 12.4% that goes into funding Social Security.

If you’re self-employed, the math is totally different. You have to pay the whole 12.4% yourself.

The formula for W-2 employees is 6.2% of whatever you’re paid that can be taxed.

The OASDI wage base is a yearly cap that limits how much of your money gets hit with that 6.2% tax. They stop taking out OASDI for the rest of the year once you earn that much. This cap goes up every year to keep pace with national wage trends.

The calculation involves taking the full 12.4% of your net earnings, not your gross income. The IRS lets you deduct half of that self-employment OASDI tax when you file your returns. OASDI is one of the biggest expenses for freelancers and small businesses.

A set percentage is taken from your earnings up to a specific yearly limit. This predictable math makes OASDI one of the easiest payroll taxes to figure out.

How OASDI Is Calculated

It seems like just a simple payroll tax, but the formula has a few parts that move around. This includes your salary and the yearly wage cap. The fact that you’re working for someone else or running your own thing is important as well.

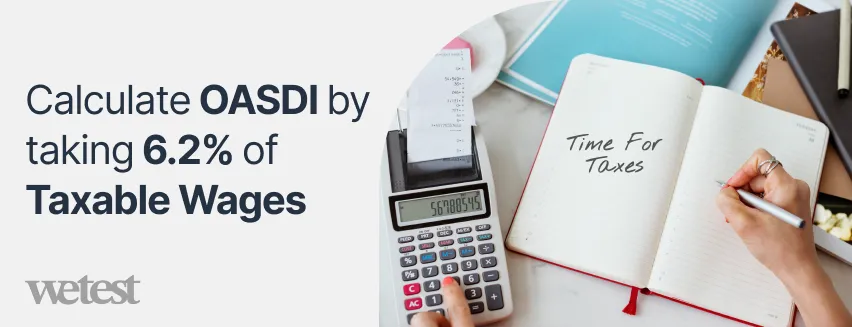

For most workers, they calculate OASDI by taking 6.2% of their taxable wages. Your manager pays another 6.2% on your behalf, so the total amount is 12.4% of your earnings. This split tax is what pays for retirement and survivor benefits.

OASDI per paycheck is always 6.2% of your gross pay, as long as you haven’t hit the yearly limit yet.

The OASDI Wage Cap

The OASDI wage base is the taxable maximum. This is the absolute maximum amount of money that’s subject to the 6.2% tax each year. They simply stop taking out OASDI for the rest of the year once your combined income hits that limit.

This cap increases every year based on how much the national average wage grows. This is why high-income people notice their take-home pay jump way up halfway through the year when the OASDI withholding magically disappears after they hit the max.

You pay the full 12.4% OASDI tax if you’re self-employed. You are allowed to deduct half of that tax on your federal return.

A lot of freelancers are shocked by how big this deduction is because OASDI is one of the largest parts of the entire self-employment tax.

Working Two Jobs?

Each employer calculates OASDI separately if you’re juggling two or more jobs.

This means you can accidentally overpay if your total income goes over the wage cap. You can claim the excess tax back when you file your tax return.

OASDI vs Medicare vs FICA

Most employees have zero idea how OASDI, Medicare, and FICA are even connected. Figuring out the difference between them makes your paycheck instantly clearer.

FICA is the actual law that forces your boss to take out OASDI and Medicare tax from your paycheck. FICA is not a separate tax at all. It’s just the big umbrella term.

Medicare tax is 1.45% plus more for high earners.

The Medicare tax funds the federal health insurance program for people 65+ and some younger people who have disabilities.

You and your employer have to pay the Medicare tax, and the rate for each of you is 1.45% of what you make.

There’s no income cap for Medicare. They hit all of your wages with it. Every single dollar is subject to this one. You’re responsible for an extra 0.9% if you’re pulling in a high salary.

Self-employed people pay taxes covering the entire cost for both sides of the equation themselves.

Common Paycheck Scenarios

OASDI is a mandatory federal payroll tax for every worker in the U.S. Your manager has to hold back 6.2% of your taxable wages to fund it.

Seeing OASDI on your pay stub just means your employer is following the law.

Sometimes people notice the OASDI amount changes between checks. The rate itself never changes. It’s always 6.2%, but your taxable wages do not! The OASDI deduction changes to match if you earn a commission or get a bonus and switch from being paid weekly to monthly. Even taking unpaid time off can make that deduction fluctuate.

A huge pain point for people with more than one job is overpaid OASDI. Each of your employers takes out tax without knowing what the others are doing. Your employer can’t fix this! You claim the excess OASDI back as a credit on your federal tax return. Most tax software handles it automatically.

Employees also search for OASDI exemptions because they wonder if they can skip the tax entirely. A few small groups are exempt. Some nonresident aliens, like student visa holders, students working for the school they attend, clergy who formally opt out, some older state government employees, and railroad workers.

Conclusion

OASDI contributions are important for your long-term financial security. Every dollar they take out is building up your eligibility for retirement benefits. This ends up being one of the most reliable income sources for millions of people later in life.

The system is set up so that while you’re working, you’re earning credits, and those credits determine if you even qualify for benefits and how much you eventually get.

You need at least 40 credits, and most people earn the maximum four credits per year pretty easily with even modest earnings. This means your OASDI payments are actively building your claim to future income.

When it’s finally time to retire, your monthly benefit is calculated using your highest 35 years of earnings, adjusted for inflation.

A lot of employees just see payroll taxes as a big expense instead of an investment. But OASDI is one of the few things you pay into that directly affects your ability to stay financially stable after you stop working.

Your OASDI money also protects you and your family through disability benefits and survivor benefits.

OASDI also matters because your contributions help keep the entire system healthy overall. The money they collect today pays for people who are currently retired, and the next generation of workers will pay for your future benefits.

A Quora Rundown

Quora discussions about Social Security contributions are personal and filled with frustrations that don’t always show up in formal explanations. Users tend to focus on the generational tension it creates and how the government handles money.

It’s not a Tax, but it isn’t Optional Either!

Some Quora users express that Social Security withholding feels like a philosophical contradiction. As John Symank puts it, “It’s not technically a tax, but you don’t get to opt out.”

He points out that participation is mandatory for anyone earning a paycheck, and that the employer’s matching contribution reinforces that compulsion.

A Generational Contract, not a Personal Savings Account

One recurring idea is that it is about supporting the generation before you, not storing money for your own retirement.

Edith Jensen summarizes this: “You’re not withdrawing your own money. You’re paying for the people who came before you, and the next generation will do the same for you.”

This social contract creates a moral dimension to the debate.

Craig Anderson notes that the program depends on the ratio of workers to retirees.

As he describes, “It takes several workers today to support every retiree, and that number is shrinking.”

How the Government Uses the Money

One of the most detailed take-downs of the system comes from Donna Forrester, and she talks a lot about her experience working in HR.

She brings up this historical change that most younger workers probably have no clue about. Back in the late 1960s, Social Security’s special, dedicated funds got merged into the general federal budget.

According to her, this totally blurred the line between what was supposed to be a protected insurance program and what just became a general source of government money.

She also points out that the government increasingly calls these benefits “entitlements,” a word she thinks carries some kind of shame. In her opinion, “People paid into it for decades, it’s not freeloading.”

The Debate Over Solvency, Debt, and the Future

Fred McGalliard writes, “A long time ago, the government realized the baby boomers weren’t going to die on schedule.” It’s a playful line with a real demographic challenge! A large generation is living longer than expected!

He predicts that the eventual fix will involve higher retirement ages or lower benefits.

Swollen Ego notes that by 2030, there will be just over two workers for every retiree, a number far lower than the ratio Social Security was built on.

The Debate Over Fairness for High Earners

Ben Gildner is a tax consultant. He explains that proposals to raise the cap change the relationship between contributions and benefits. His concern is structural:

“It breaks the link between what you pay in and what you get out, and that’s when the system stops being insurance and starts being welfare.”

Turning Social Security into a redistributive program could threaten its long-term political support. To him, Social Security’s strength is that everyone feels they earned their benefits.

Social Security as a Safety Net

Some users use philosophical arguments to push back on the whole idea that Social Security should pay for a comfortable retirement. They just don’t think that’s what it was designed to do.

Karl D sees the whole thing as insurance that’s only supposed to “fill the holes, not build the road.”

His basic point is that Social Security is meant to stop people from being completely poor in their old age, not to guarantee everyone a middle-class lifestyle.

FAQs

Are OASDI and Social Security the same thing?

Yes. OASDI stands for Old-Age, Survivors, and Disability Insurance, the official name of the Social Security tax. It is the tax withheld to fund Social Security benefits.

How much OASDI will be withheld from my paycheck?

OASDI is withheld at a rate of 6.2% of taxable earnings, up to the annual wage base limit. Employers match that with another 6.2%.

Why did the OASDI deduction suddenly stop on my paycheck?

Once your year-to-date earnings meet the annual Social Security wage base, withholding of OASDI stops automatically for the rest of the year.

What happens if I work multiple jobs and pay too much OASDI?

Each may withhold OASDI independently, which can lead to overpayment when combined wages exceed the annual cap. This is refundable when you file your federal income tax return.

Can I opt out of paying OASDI tax?

Specific religious sect members or clergy who formally opt out, or certain local government employees covered under alternative retirement systems, qualify for exemption.

If I’m self-employed, do I still pay OASDI?

Yes. You should pay the full Social Security tax, currently 12.4% on net earnings.

Hire the best candidates

with Wetest.

Create pre-employment assessments in minutes to screen candidates, save time, and hire the best talent.

Try for free